- R.F.'s Financial Newsletter

- Posts

- This Week in Barrons: 03.08.2026

This Week in Barrons: 03.08.2026

Heads you win - Tails I lose...

R.F. Culbertson

March 08, 2026

In partnership with

—To subscribe: https://rfsfinanicalnews.beehiiv.com/subscribe

Lux Capital warned its founders to prepare for rising business risk... noting that 10-year yields are falling alongside near-record stock prices. This historically has signaled an oncoming recession. The firm advised founders to:

o Extend their cash runway,

o Review their venture-debt covenants, and

o Cut costs – especially tariff-sensitive imports.

Memos such as this typically appear when the investing cycle turns lower. Similar warnings came in 2022 after the end of our FED’s Zero Interest Rate Policy and early in the pandemic. While AI valuations remain elevated, private markets usually reprice slowly – through reduced funding, smaller exits, and multi-quarter strategy shifts. As a result, VCs are rotating toward infrastructure, credit, and secondaries that deliver more predictable cash flow rather than long-duration growth bets.

Seth Godin argues that education... trains people for process-driven, factory-style tasks, all-the-while suppressing imagination. As AI automates routine work, imagination and original thinking may become the key differentiator in future employment.

The Markets:

Key market signals that are often missed:

o Hormuz risk isn’t about $80 oil, but whether a sustained risk premium resets inflation expectations and the rate curve.

o Data centers can trip our power grid’s offline signal instability by generating a demand spike. This will affect how AI infrastructure gets financed moving forward.

o The AI–Pentagon dispute is less about ethics and more about federal risk, blacklisting exposure, and regulatory leverage over frontier tech.

o Blue Owl Capital’s stress reflects liquidity promises colliding with market pricing after assuming retail capital would behave like institutional money.

o For private markets, rising inflation risk and policy uncertainty push discount rates higher before credit spreads widen.

Oil will determine whether Iran becomes an economic problem: If crude stays elevated, the conflict will shift from geopolitics to a household tax. Energy shocks typically hit the economy not via supply shortages but by squeezing consumer spending. After all, higher gasoline prices will reduce disposable income. My question for next week is whether the new economic data we receive - support last week’s shift toward patience and cash flow, push investors back toward growth, or cause ‘Panic at the Disco’?

Things I’m Reviewing… the interesting ways that Cheers builds your credit … R.F. Culbertson

Your Credit Could Be Worth $200,000

Guess how much good credit can save you?

Up to $200,000 over your lifetime, according to Time Magazine.

Better credit means lower rates on mortgages, auto loans, and more. Cheers Credit Builder is an affordable, AI-powered way to start building credit — even from scratch. No credit score required and no hard credit check — just a quick ID verification.

Choose a plan that fits your budget, link your bank account, and make simple monthly payments. We report to all three major credit bureaus with accelerated reporting to help you build credit faster.

Many users see their credit scores increase by 20+ points within a few months, helping them prepare for goals like buying a home, leasing a car, or qualifying for better rates.

Your funds are FDIC-insured through Sunrise Banks, N.A., and returned at the end of your plan (minus interest). Cancel anytime with no penalties.

Start building smarter today — your future self could thank you six figures later.

Info-Bits…

Waymo taxis are under review: Autonomous vehicles from Waymo in Austin, failed to stop for ~24 school buses and even once blocked an ambulance. This raises concerns about how they interpret risk.

Oil signals the equity bottom: In major Middle East conflicts, stocks often bottom the same day oil peaks – making energy markets the key inflection indicator.

February Jobs... were down -92,000 – the third drop in five months. Adjusting for the +90,000 additions by the Birth/Death model (fake jobs), the underlying loss was about -182,000 jobs.

Tariff refunds: a federal court ordered $130B+ returned in voided tariffs. This restored liquidity to importers and potentially shifted market behavior quickly.

iPhone 17e started selling at $599... It runs on-device Apple Intelligence, includes A19 chip, 256GB base storage, Call Screening, Hold Assist, and Live Translation.

A DHS breach was claimed by hacktivist group... the Department of Peace. They accessed DHS’s data and leaked ICE-related information tied to ~6,000 vendors, including Anduril Ind., Palantir Technologies, Microsoft, and Oracle.

The Luxury sector is under pressure: Shares of LVMH, Kering, and Burberry are falling as the Middle East conflict weakens a key sales region.

“Send in the Kurds”... is a plan for the U.S. to arm Iranian Kurdish opposition groups to help trigger an uprising against Tehran. [FYI: ‘Send in the Kurds ... They’re ought to be Kurds ... Don’t wait till next year.’]

Crypto & AI-Bytes:

Anthropic is nearing a $20B annual revenue run rate... up from $9B at the end of 2025, before the Pentagon labeled it a supply-chain risk.

Amazon said Middle East drone strikes damaged AWS data centers... in the UAE and disrupted a facility and caused outages in Bahrain.

OpenAI amended its Pentagon contract... adding language banning domestic surveillance of U.S. citizens and excluding agencies like the NSA.

Deveillance launched Spectre I... a portable device that masks speech from microphones within ~2 meters.

OpenAI launches GPT-5.4 with built-in computer use and a full financial services suite: It is the first general-purpose model that can click, type, and navigate software to complete multi-step workflows autonomously. The release also features ChatGPT for Excel in beta, embedding the model directly into spreadsheets.

Prediction markets Kalshi and Polymarket... are raising funding at ~$20B valuations – roughly double late-2025 levels.

Things I Read… This FREE Fintech Newsletter is certainly worth the read … R.F Culbertson.

Most coverage tells you what happened. Fintech Takes is the free newsletter that tells you why it matters. Each week, I break down the trends, deals, and regulatory shifts shaping the industry — minus the spin. Clear analysis, smart context, and a little humor so you actually enjoy reading it. Subscribe free.

Morgan Moment(s): Q & A…

Mark Cuban will judge the Forge AI Prize... during NFL Draft week (April 22) in Pittsburgh. AI founders building sports and robotics tools will compete for $1.275M – including $1m in AWS compute credits and a $275k investment from Magarac Venture Partners. The Judges are Cuban and Ed Stack.

Coding Commoditization: AI-driven software creation and “vibe coding” are lowering barriers to building-your-own software and raising fears of new startup competitors. But this ignores that software firms themselves can use AI to boost productivity in a labor-intensive industry. It also underestimates the durability of incumbents – their distribution, scale, and brand advantages – further suggesting that software’s “death” may be overstated and premature.

Take Away the Water Supply: A single precision strike on a major Middle Eastern water facility will cripple a nation instantly. Countries can’t survive without water. All sides know where these plants are, yet they aren’t targeted. This suggests to me that the goal may not be annihilation but pressuring neighbors away from further U.S. alliances..

Next Week... Heads you win, Tails I lose…

Last Week’s Sentiment:

Markets nearly capitulated Tuesday... but the SPX 6,750 level held. If geopolitics cool off, a snap-back rally toward 7,000 is possible.

BlackRock allowed limited redemptions in their private credit fund... while Blackstone was doing something similar only being down ~30% YTD. This highlights the liquidity stress in private markets.

CBOE Volatility Index spiked to a 9-month high... and the VVIX jumped 17%. The volatility curve flipped to backwardation (40-day vol > 74-day). This is rare with the market only ~4% off all-time highs.

February Jobs shocked: losing -92,000 jobs vs gaining +55,000 that was expected. Adjusting for the Birth/Death model (+90K) implies ~-182,000 jobs. [FYI: Hey, what’s a -250,000 job-loss among friends.]

A short-term bounce is possible... but volatility structures signal elevated risk through the end of next week.

Last Week’s Facts:

The SPX closed within 4 points... of its weekly expected-move’s lower bound. That shows unusually tight pricing on a ~7,000-point index.

Next week’s SPX expected move jumped to $226... up from (from $144) – with volatility rising another ~10% late Friday.

The VIX finished at ~27.5... and historically this is where volatility turns into a ‘fade’ or accelerates toward 35 – 40.

iShares iBoxx $ High Yield Corporate Bond ETF is weakening... though not yet reflecting the stress seen in private credit.

The deeper market risk may be... mispriced valuations and capital mis-allocation – driven by storytelling rather than durable earnings.

TIPS...

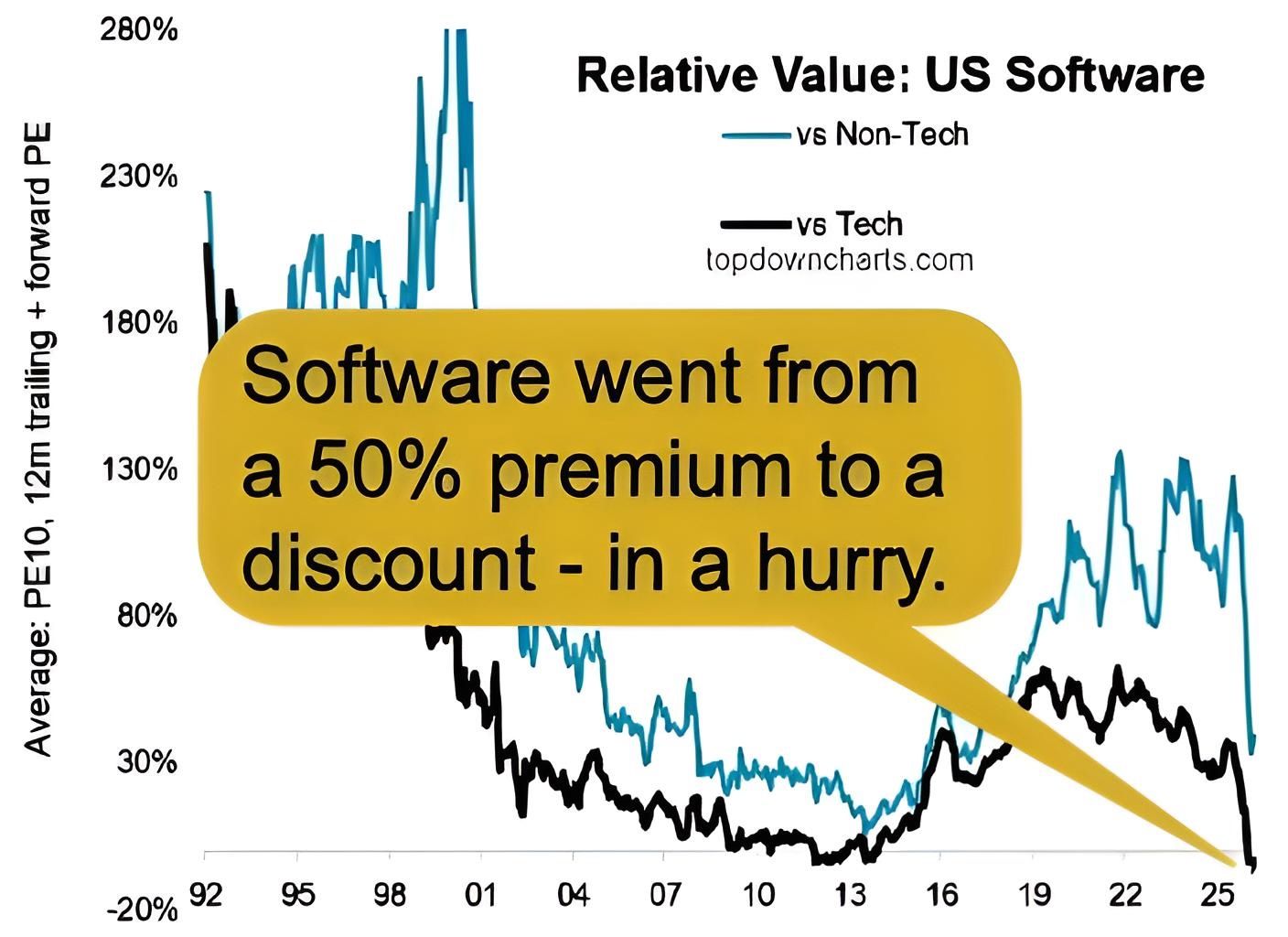

Factually... (a) The S&Ps have broken a key short-term support level – granted from a point of stretched sentient & valuations; therefore, risk of further downside is elevated. (b) Software stocks are bouncing from cheap and oversold conditions. And (c) Energy stocks are getting a geopolitical boost with room to run. Overall, per Cullum Thomas: The technical picture is enough to make one pause and think. With the various parallels to 2022, this certainly heightens the risk management senses. And yet there remain some very interesting sector setups.

Trading TIPS = Last Week’s BIG BUYS:

o Tip #1: SPDR Gold Shares (GLD) = Bullish: 110,676 new +$495 / -$510 Call spreads (exp. Mar 27) were purchased at the ‘ASK’. They’re targeting a $510 retest within ~3 weeks.

o Tip #2: Schlumberger (SLB) = Bullish: ~10K contracts rolled their $55 Calls to $50 Calls (exp. May 15). Raising the delta like this (22% to 40%) signals a strong conviction despite energy weakness.

o Tip #3: KWeb shares (KWEB = CSI China Internet ETF) = Bearish: +$27 / -$25 Put spread with $35 Calls sold (exp. Jun 18). Chinese technology is positioned as a downside trade.

o Tip #4: SoFi (SOFI) Technologies = Bullish: 110K calls rolled from +$19 / -$22 to +$20 / =$23 (exp. Mar 20). This effectively lifts the price target as markets weakened.

o Summary: Bullish gold, oil services, and fintech; Bearish China tech– with a strong dollar driving the theme.

HODLs: (Hold-On for Dear Life):

- Holding / Reducing:

o (-) Ethereum (ETH = 1,989 / in at $310)

o (-) Bitcoin (BTC = $67,400 / in at $4,310)

- Increasing:

o (+) Physical Commodities = Gold @ $5,181/oz. & Silver @ $84.6/oz.

o (+) SLV (silver ETF) == ($75.9 / in at $27)

o (+) GLD – Gold ETF ($473.5 / in at $212)

o (+) GDX (gold miners ETF) == ($101.3 / in at $52)

o (+) SIL (silver miners ETF) == ($101.2 / in at $86.05)

o (+) COPX (copper mine ETF) == ($79.9 / in at $55.3)

o (+) CCJ (uranium) == ($109.6 / in at $84)

o (o) ATXRF (small copper & gold miner) == ($2.7 / in at $2.47)

o (o) FMANF (small gold miner) == ($0.26 / in at $0.17)

o (+NEW) ITRI (Itron, the grid’s intelligence layer) == ($91 / in at $96)

o (+NEW) MTZ (MasTec, the grid’s builder) == ($285 / in at $268)

o (+NEW) PWR (Quanta Services, king of the grid) == ($540 / in at $525)

o (+) EWY (S. Korea ETF) == ($126.7 / in at $120.81)

o (o) QQQI (13% covered-call, QQQ’s divi. producer == pay mo.)

o (o) ICSH (short term bonds = 4.65% yield == pay mo.)

Please be safe out there!

Disclaimer

Expressed thoughts offered within the BARRONS REPORT, a Private and free weekly economic newsletter, are those of noted entrepreneur, professor and author, R.F. Culbertson, contributing sources and those he interviews. You can subscribe by visiting: https://rfsfinanicalnews.beehiiv.com/subscribe.

Please write to Mr. Culbertson at: <[email protected]> to inform him of any reproductions, including when and where copy will be reproduced. You may use in complete form or, if quoting in brief, reference <http://rfcfinancialnews.blogspot.com/> and/or https://rfsfinanicalnews.beehiiv.com

If you'd like to see R.F. in action - please feel free to view the TED talk that he gave on Fearless Investing.

Creativity = https://youtu.be/n2QiPSe_dKk

Sales = https://youtu.be/blKw0zb6SZk

Startup Incinerator = https://youtu.be/ieR6vzCFldI

To unsubscribe please refer to the bottom of the email.

Views expressed are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest and is not in any way a testimony of, or associated with Mr. Culbertson's other firms or associations. Mr. Culbertson and related parties are not registered and licensed brokers. This message may contain information that is confidential or privileged and is intended only for the individual or entity named above and does not constitute an offer for or advice about any alternative investment product. Such advice can only be made when accompanied by a prospectus or similar offering document. Please make sure to review important disclosures at the end of each article.

Note: Joining BARRONS REPORT is not an offering for any investment. It represents only the opinions of RF Culbertson and Associates.

PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING. WHEN CONSIDERING ALTERNATIVE INVESTMENTS (INCLUDING HEDGE FUNDS) AN INVESTOR SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS AND OTHER SPECULATIVE INVESTMENT PRACTICES MAY INCREASE RISK OF INVESTMENT LOSS; MAY NOT BE SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

Alternative investment performance can be volatile. An investor could lose all or a substantial amount of his or her investment. Often, alternative investment fund and account managers have total trading authority over their funds or accounts; the use of a single advisor applying generally similar trading programs could mean lack of diversification and, consequently, higher risk. There is often no secondary market for an investor's interest in alternative investments, and none is expected to develop.

All material presented herein is believed to be reliable but we cannot attest to its accuracy. Opinions expressed in these reports may change without prior notice. Culbertson and/or the staff may or may not have investments in any funds cited above.

To Subscribe: https://rfsfinanicalnews.beehiiv.com/subscribe

Remember the Blog: <http://rfcfinancialnews.blogspot.com/> and/or

https://rfsfinanicalnews.beehiiv.com.

Until next week – be safe.

R.F. Culbertson